The new year brings three new reasons to make CGAs the centerpiece of your planned giving marketing program in 2023: New payout rates, new discount rates, and the new Legacy IRA.

Let’s take a look at what’s changed — and how those changes will benefit your donors.

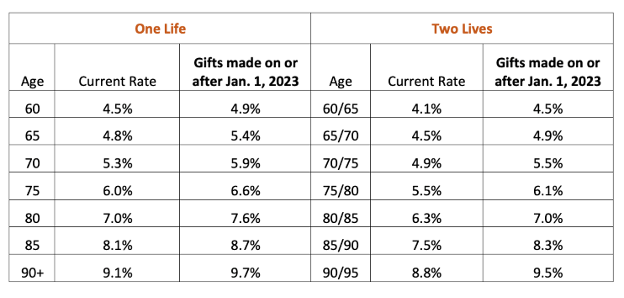

1) New CGA Rates

New recommended payout rates went into effect on Jan. 1. It’s the second rate increase in six months. On average, payout rates will increase about 0.6 percent over the rates that went into effect on July 1, 2022.

This chart shows a comparison:

2) Increased IRS Discount Rates

The IRS has been steadily increasing the monthly Section 7520 Rate, used to calculate the present value of long-term assets such as charitable gift annuities. Higher rates correspond with larger tax deductions for the donor. In January 2022, the Section 7520 Rate (also called the Discount Rate) was 1.6 percent. In January of ’23, the rate reached 4.6 percent — and that increase results in substantial tax savings.

For example:

If Mary Donor, age 77, had made a $50,000 contribution to an Immediate CGA in January 2022, her CGA payout rate would have been 5.8 percent, and her IRS Discount Rate would have been 1.6 percent, yielding her a $24,023 charitable tax deduction.

But if Mary were to make a similar \$50,000 contribution to an Immediate CGA today, the results would be substantially different. Her CGA Payout Rate would rise to 7.0 percent, and her IRS Discount Rate would jump to 4.6 percent, yielding her a charitable tax deduction of \$23,880.

While the deduction dropped only slightly, her CGA Payout Rate rose from 5.8 percent to 7 percent. Normally, that would have greatly reduced the charitable tax deduction because under the 7 percent payout rate, Mary would receive $53,550 if she lives to life expectancy, versus $44,370 under the old 5.8 percent payout Rate — leaving less to go to charity at her death.

However, with the dramatic increase in the IRS discount rate over the last year, Mary’s charitable tax deduction is just $143 less, but she can expect to receive $9,180 more in annuity payments over her lifetime! This is an incredible benefit!

3) The new LEGACY IRA is here

Over the last decade, the nonprofit community has lobbied Congress to allow donors who are required to take taxable Required Minimum Distributions (RMD) annually from their IRA accounts to use part or all of those RMDs to fund a split interest gift device, such as a Charitable Remainder Trust (CRT) or Charitable Gift Annuity (CGA). On Dec. 23, 2022, Congress finally listened, passing the Secure Act 2.0 as part of the Consolidated Appropriations Act of 2023.

A portion of the Secure Act 2.0 created the new Legacy IRA. This means that a donor over 70 ½ can use their RMD as a Qualified Charitable Distribution to fund a gift such as a charitable remainder trust or charitable gift annuity in an amount up to $50,000 and not suffer a tax penalty. Previously, lifetime distributions from an IRA account were not allowed to fund a CGA.

This allows donors over 70 ½ to use part of their IRA to make a Planned Gift in the form of a CGA to produce lifetime income for themselves, with the remainder going to their favorite charity at their death outside their estate.

These three events coming together in 2023 are likely to make the stodgy old CGA the new darling of the gift planner’s offerings. The donor benefits are even more attractive than before, so if your nonprofit is not currently offering CGAs, now is the time to start!

For more information, contact jsyverson@magnifyyourimpact.com or call (515) 277-4050 to schedule a call.